{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

9 years ago

Ethics of Subprime Mortgages

By James Smith

There are few individuals throughout the United States and in worldwide business who do not know what Subprime mortgages are and what effect they have had on the worldwide economy. Subprime mortgages can essentially be defined as loans given to individual with insufficient qualifications with an impossibility of being paid back. When the world started to realize these mortgages were going to have detrimental effects on the world’s economy the loans couldn’t even be distinguished because they had been bundled and sold so many times (Barnes). Why were these loans made? Why did people accept them? Was it ethical to make these loans?

These loans were given and accepted for many reasons; in 2002 the economy began to rapidly expand, home values began to rise dramatically and interest rates were very low. It also seemed that the American dream of owning a house was attainable for anyone willing to sign on the dotted line, even for those with little or no down payment and often less than ideal credit. These mortgages were often lent with the adjustable rate attached to the loan, which showed low monthly payment; unfortunately it was only temporary. Many banks made these loans without enough hesitation because they were securing most of their profits on the front end of the loan; the individuals taking out the loans figured the value of their home would never stop increasing they had nothing to loose (Barnes).

Thomas Kostigen from marketwatch.com states “Exploiting those in need never gets any one ahead of the game in the long run. Sure, short-term profits are there to be made, but ultimately repentance prevails.” He said this in an article he wrote about subprime mortgages and the ethics involved around them. This statement seems to sum up the whole cycle of the affects of these types of loans, yes there was much money made on these loans, but now, in the long term many people and entire companies are paying the price. Kostigen also warns about companies that scheme for quick money typically do not have a solid ethics base vs. good performance comes from good ethics throughout companies.

In contrast to poor ethical decisions made by many banks John Allison, recently retired CEO of BB&T ( a bank based in NC with around 1,500 branches and 143 billion in assets (Hemingway)) explains “Subprime mortgages were bad for the people who took them out. That went against BB&T’s philosophy.” This bank has been able to stay out of financial trouble and away from government money by following its solid time proven philosophies. Allison is still out to make money and is a supporter of capitalism but he has shown through his actions that one is better off in the long run being honest; and looking out for both the company and the clients yields better profits and relationships in the future.

Now that the dust has settled perhaps individuals both involved and those who watched from the sidelines will take another look of how important ethics are. People are in business to obviously make money and it seems that those who had strong principles and ethics did just that.

References:

Barnes, R. (n.d.). The Fuel That Fed The Subprime Meltdown. Retrieved November 18, 2009, from Investopedia.

Hemingway, Mark. "Objectivist Philosophy for Fun and Profit." National review online. 30 Apr. 2009. Web. 5 Dec. 2009.

Kostigen, Thomas. "No surprise here Shaky ethics of subprime lending lead to shaken investors." Market Watch. 27 July 2007. Web. 6 Dec. 2009.

Property Management-- Mike Kremko, Mark Silva, and Daniel Fiero

Real estate can be used for its investment value including apartment complexes, offices, or shopping centers. For property owners it is often necessary to hire a property manager to supervise the operation since it can be tedious and the property may often be located in a different city. The property manager has duties including: accounting, maintaining equipment, accepting rent, and responding to any issues a tenant may have. A property manager may be a licensed real estate salesperson, but generally they work under a licensed real estate broker. They act as a buffer between property owners and tenants. Should any issues arise, the property manager will more than likely bring them to the attention of the property owners in an attempt to remedy the issue, but some issues can be easily resolved without the owner’s involvement. We will be discussing property management from the landlord’s point of view covering such things as possible income properties, the job of a property manager, perspective tenants, and contracts with tenants.

Residential Property Management

Screening prospective tenants is an important thing a landlord should always do to protect their investment and to also prevent any unnecessary problems. Since the turnover rate is typically high in the residential market, it is best to do a thorough check to prevent a vacant unit and any legal issues. One of the first things to do is have them fill out a rental application. Be sure to get full names, copy of their driver’s license/identification card, social security numbers, and employment history with a recent check stub. A small fee should be charged to cover the expense of checking their credit report, which can now be done easily on various websites at a small fee. Getting a credit report will determine if the prospective tenant has been consistent about paying their bills and their debt to income ratio is not too high. If they have met your criteria, it may be reasonable to think the perspective tenant will be able to pay you the amount agreed for the duration of the lease. If they have not been responsible in the past, it may be a risk to assume they will pay you and will either require you to choose the next applicant or require a cosigner for the current applicant. Next it is crucial to get fairly recent references. If possible, get numbers to old landlords and speak with them. This will be a good way to get their rental history or learn of any issues they may have had in the past (Haupt & Dorsey). At this point you would want to schedule an appointment with the prospective tenant to explain your expectations of them. This will provide a way to see how they react to those expectations. Also, it invites questions from both sides to clarify any ambiguity. Once terms have been agreed on and the interested party decides on the property, it is time to sign a lease agreement.

A lease agreement must comply with state and local laws. Depending on the area, lease agreements may have some differences. It is a good idea to have an attorney review your lease to make sure it is compliant with local and state laws, as well as enforceable in court. The lease will all have some major components such as: name of tenants, lease term (typically one year), payment of rent, deposit, fees, user responsibilities, pet clause, security deposit clause, and access to premises (Lopez). The lease will also include information on what will happen if the tenant is late on a payment or if they refuse to pay.

In California the eviction process is complicated and sometimes costly. The eviction process begins with a 3-Day Notice to Pay or Quit, 30-Day Notice to Vacate, or 60-Day Notice to Vacate (Marsh). If the tenant doesn’t move out by the specified times, the landlord may file an unlawful detainer. In an unlawful detainer, the landlord is the plaintiff and the tenant is the defendant. Usually within 1 to 10 days the tenant is served with summons papers. At this point it may be a good idea for the tenant to seek legal advice. The legal process is very complicated and lengthy. In the end the court could rule in favor of the tenant. In which case, the tenant may continue to reside in the rental unit and the courts may award the tenant his legal fees as well as damages. The court could also rule in favor of the landlord. In this case, the court orders a “writ of possession” and awards the landlord legal fees and unpaid rent. The court clerk will issue the order to the Sheriff. Within 1 to 3 days a peace officer will deliver a 5 days’ notice to vacate the property or be evicted. If the tenants do not comply the peace officer will physically remove the tenants and return the property to the landlord’s possession. Although the eviction process rarely occurs, it is best to understand how to handle the process.

Commercial Property Management

Screening perspective tenants in commercial real estate differs for the process done in residential. Unlike residential properties, there is a fairly low turnover rate in commercial properties because businesses become synonymous with a certain location. Property management companies usually will put together a detailed packet of information for potential renters, which include traffic studies, demographics of the area, and land reports. Due to the troubled economy the turnover rate has gone up in commercial real estate and there are more vacant storefronts and office buildings in cities across the country. When applying for a commercial space a few more factors are taken into consideration. A typical application will have you include a full balance sheet of the company, any liquid assets or collateral possessed by the company or their owners in the event that the rent is not paid, and information on any cosigners of the property. Additionally, the perspective tenant will have to have either enough cash or a loan from a banking institution in order to complete any work on the property. Once the application has been processed and accepted, the lease agreement is covered.

Unlike residential leases, a commercial lease will be a long-term contract with various different clauses. One main difference between residential and commercial is that the commercial property is leased out by total square footage and could also have additional monthly fees based on their monthly income. Another clause in the lease is a tenant improvement allowance or TI allowance for short. Many commercial properties are leased as an open floor plan, which allows for tenants to design their property in a way that is beneficial for their business. A tenant improvement allowance is usually given once the work is complete and is paid out by the owner per square foot. The tenant improvement allowance covers the construction costs of any fixed items that will continue to be in the property after the tenant leaves (Schwellinger). Typically with a commercial lease, the repercussions of defaulting are much greater. The property owner could keep the security deposit, restrict you from entering your property, and will more than likely sue you for all rent for the duration of the contract.

California Eviction Guide For Tenants and Landlords

Prepared By: Melissa C. Marsh, Los Angeles Landlord-Tenant Attorney

http://www.ehow.com/articles_4827-property-management.html

Schwellinger, Brian. "Questions and Answers about Tenant Improvement Games." 20 APR 2005. Web. 20 Nov 2009. http://www.realestatedec.com/artman/publish/article_49.shtml

Haupt, Kathryn, and Megan Dorsey. California Real Estate Practice. 4th. Rockwell Publishing, 2009. Print

Lopez, Carrie. "A Guide to Residential Tenants’ and Landlords’ ." July 2006. California department of consumer affairs, Web. 18 Oct 2009.

http://www.dca.ca.gov/publications/landlordbook/catenant.pdf

be successful in reaching an agreement.

be successful in reaching an agreement.

There are many different ways to finance your home and in today’s economy it is key that you find the best mortgage that will fit you. First you must asses what type of loan you are looking for or if you qualify for government aid when financing your home. You must take in consideration the time duration that you plan on living in your home or if it is just a business investment.

If as a home buyer you are able to qualify for a Federal Housing Authority loan or FHA loan, you then might want to take a good look at this type of loan because it can be very beneficial for the buyer. This type of loan typically targets new home buyers because the payments for this loan will require smaller down payments than typical loans from other lenders. The terms of these loans are usually set for 30 years and are targeted for purchases around moderately priced homes. One draw back is meeting the qualifications of this type of loan but if as a home buyer you are able to get this type of loan it could be a very appealing loan. According to http://www.fha.gov/ they have insured more than 37 million mortgages since the year 1934.

If as a home buyer you are able to qualify for a Federal Housing Authority loan or FHA loan, you then might want to take a good look at this type of loan because it can be very beneficial for the buyer. This type of loan typically targets new home buyers because the payments for this loan will require smaller down payments than typical loans from other lenders. The terms of these loans are usually set for 30 years and are targeted for purchases around moderately priced homes. One draw back is meeting the qualifications of this type of loan but if as a home buyer you are able to get this type of loan it could be a very appealing loan. According to http://www.fha.gov/ they have insured more than 37 million mortgages since the year 1934.

NAMING YOUR PRICE

How to Evaluate and Price Your Home

Michael Efird, Patrick Darnell, Kathy Xiong

(www.atlantabesthomes.com/images/pricing.jpg)

You need to sell your home and you have no idea what your house can sell for. Deciding on a selling price for your home is not an easy task in any market. In a seller’s market you might be nervous of “leaving money on the table”. In a buyer’s market you might be concerned with overpricing that could result in not selling at all. Even in a stable market there is the balance of maximizing price with how fast you want to sell. However is there really such a thing as a stable market in California? It tends to be traveling one way or the other.

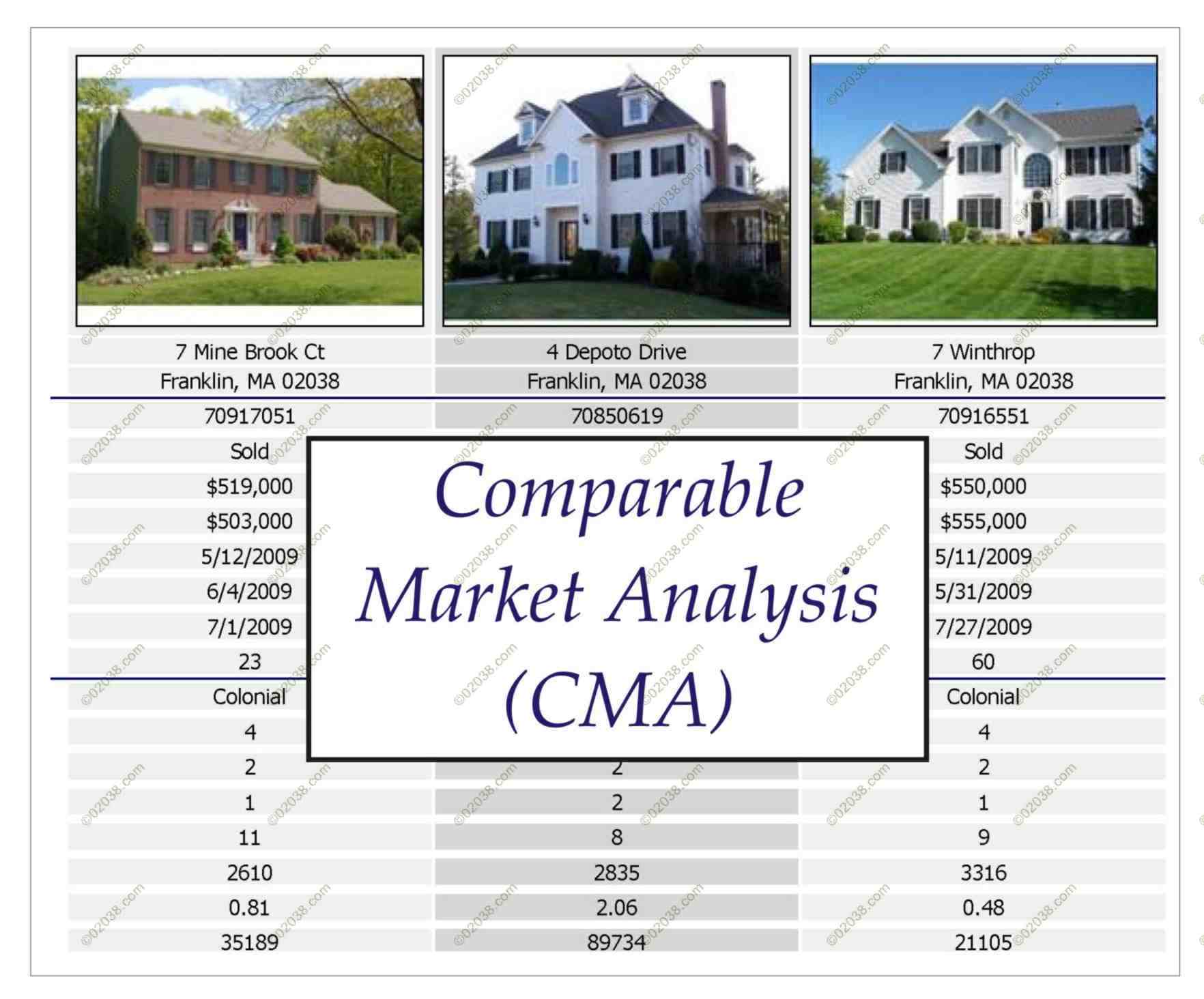

There are several different methods that can be used to calculate your home’s value and selling price. There is the eyeball method, website calculation, and a CMA (Comparable Market Analysis) from a real estate professional. All of these are methods that are used by homeowners to sell their home. We will discuss each of these and provide explanation on which method you should use and how to insure that method is done correctly.

In the Eyeball method a homeowner does a survey of their surroundings. They take inventory of the houses in their neighborhood for sale. They make a rough assessment on the condition of the houses for sale. Then the homeowner compares the listing prices of the homes in the area along with their condition and derives a value of their own home in relation to the other homes. This method is flawed in many ways. This method only takes into account what houses are listing for and not they are selling for. This method also is based more on personal value and not on what the market will truly produce. Most importantly this method is not being performed by a professional in real estate. In this method there is high probability that your home will not be correctly priced due to the subjectivity involved.

(http://www.sterlingrealestateinvestments.com,/ 2009)

The website method has become widely used. The age of the internet and information now has driven several websites to do the calculation for you. A popular website for this is Zillow.com. Zillow.com provides you with what is called a zestimate. This is Zillow’s estimate of what your home’s value is. These websites take the personal aspect out of home pricing which is dominant in the eyeball method. The website methods take a straight statistical approach to home values. They take the most recent sales available within a reasonable distance and populate those into a data base along with their square footages. This gives them a price per sq ft. this price per sq ft is then applied to homes of similar size. This method has some perks. The first is time; you can have a “Zestimate” in seconds. You literally can drive around neighborhoods with your IPhone and research home values instantly. This method also uses actual home sales where the eyeball method uses listing price. This method is purely objective not subjective. It merely takes the statistical data of actual events and calculates what your home is valued at. There are some pitfalls to this method. Typically these methods undervalue the property because they do not take into account items that can increase the value of the home. These websites do not take into consideration pools, garage sizes, R.V. parking, condition of home, or other items that will directly influence the amount the home will potentially sell for. In the example given below three houses next to each other have the following values, $241,000, $240,000, and $212,000 (http://www.zillow.com/homes/2814-W.-Newton-Ct.-Visalia,-CA_rb/). The least expensive home is 1,869 sq ft. with price per sq ft of $113. The other two houses are both 2,675 sq ft. with a price per sq ft of $90 per sq ft. The house priced for $240,000 has a large lot, fire pit, R.V. parking, custom cabinets, and many upgrades. The home priced at $241,000 does not have these features yet is valued at a $1,000 more. There is also the difference of $23 per sq. ft. between the other two houses. This method typically does not have the most current data. This method is typically three months behind, according to Marc Paolella of trulia.com. Which in a fast changing market could turn out to be disastorous? This method is getting better as technology and GIS systems improve. However at this time it is not the most accurate best way to price your home. (Paolella, 2008)(zillow.com, 2009)

(http://www.02038.com/, 2009)

The third way is to have a Realtor provide you with a CMA (Competitive Market Analysis). This method is the most comprehensive way of calculating a pricefor your home without paying an Appraiser. This method takes into account all of the processes of the other two methods and expands on it. The CMA is broken into four steps:

· Collecting and Analyzing information about the sellers property

· Choosing the Comparable Properties

· Comparing the sellers property to the comparables and adjusting values accordingly

· Estimating a realistic selling price.

When collecting information about the seller’s property the Realtor will begin by analyzing the seller’s property, neighborhood, and the structure itself. The Realtor will be looking for things that may increase or decrease the value of the home. These items may include the location in regard to schools and shopping, the condition of the other homes in the neighborhood, the condition of the property, and the condition and layout of the home itself. The Realtor will then locate comparable properties both for sale and sold within the same neighborhood. These comparables are adjusted to match the subject property. This is done by adding or subtracting the value of the different amenities and or features that create value. (National Association of Realtors, 2009)

Once this is completed the Realtor provides an estimate of a realistic selling price. At this point the homeowner can make an informed decision on what they would list their home for. This process incorporates not only statistical information but also takes into consideration the subjective information. In interview with Jayne Wills, a Realtor in Visalia, she stated:

“The key to this approach is using both sold and for sale comparables. You need to make sure you price your home competitively but also at a price that is line with homes that are actually closing on the back end.” She went on to say, “it is important that you are using all information that is available to Appraisers. You have to be able to appraise the home for what it sells for or you could lose the sale when the appraisal is less than the selling price.” -Jayne Wills, 2009

This means that the CMA will need to most likely include any foreclosures or short sales. All comparables need to be used with caution. You will not want to use sales that are not typical of the other sales. For instance if the neighborhood has a significant amount of foreclosures and short sales, it would be necessary for them to be included. If there are few of these, then they might be excluded as comparables but still included as part of the CMA.(Wills, 2009)

The Realtor CMA is the best method for pricing your home. However it is not without its own potential drawbacks. The CMA is reliant upon the Realtor performing ethically and in the best interest of the Principle. Sometimes a Realtor might be more interested in a quick sale or in a large commission. In these cases it is possible for a realtor to act unethically by including comparables that slant the CMA one way or the other. This can be avoided by having several Realtors provide you with a CMA before you decide which one you want to sign a contract with. By doing this you can get several perspectives and decide which one works best for you. At the fallowing web address you can find a good example of what to expect in a CMA, http://www.homepricelv.com/SampleCMA.pdf.

Selling your home is not an enjoyable task for most people. It is important that we avoid unnecessary pitfalls and stress during this process. The best way to do this is to use a Realtor and have them provide a CMA so that you will be well informed when deciding how to price your house.

References:

www.atlantabesthomes.com/images/pricing.jpg

NATIONAL ASSOCIATION OF REALTORS CODE OF ETHICS-evaluating and pricing, Chicago, IL. 2009 http://www.realtor.org/MemPolWeb.nsf/pages/COde

Paolella, Mark 2009 http://www.marcpaolella.com/

www.trulia.com/voices/homebuying

Wills, Jayne: Remax Real Estate Agent, Interviewed by Patrick Darnell, 2009

http://www.zillow.com/homes/2814-W.-Newton-Ct.-Visalia,-CA_rb/

http://www.02038.com/wp-content/uploads/2009/09/nego-price-home-for-sale-MA-9.jpg

http://miamiangelproperties.com/blog/short-sales-101.htm for image on the right.